Smart money starts young: building financial discipline from childhood

Children learn fast, sometimes faster than we’re ready for. The habits they pick up early often stick with them for life. That’s why money habits shouldn’t wait until adulthood, when bad patterns are already harder to unlearn. Many adults struggle with saving, budgeting, and delayed gratification simply because no one showed them how when they were young.

Financial literacy isn’t something most people magically “figure out” later. It’s something they either grow into or struggle without. This is why it’s often easier to build positive money habits in children than to correct poor financial behaviours in adults who were never taught growing up.

The foundation can start as early as primary school, when children begin grasping simple concepts like choices, rewards, and waiting.

Why starting early matters

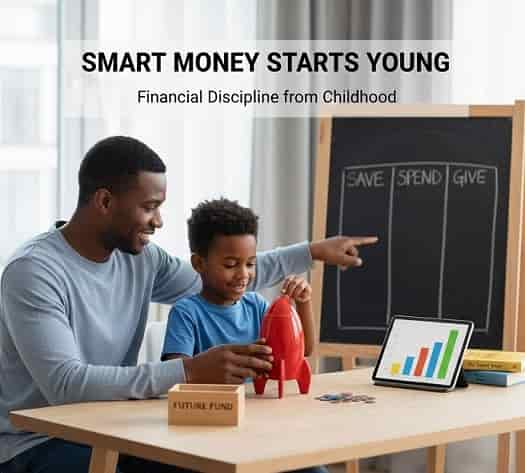

From a developmental viewpoint, children begin forming habits and behavioural patterns as early as ages 2–3, when they start learning through routines, imitation, and simple cause-and-effect.

Once they can observe, mimic, and ask questions, they’re learning how the world works. Teaching money at this stage doesn’t mean introducing compound interest to a toddler, it means simple lessons like waiting, choosing between options, and understanding that money is limited.

Early exposure builds a balanced relationship with money. Instead of seeing it as something that simply appears on demand, they learn it’s earned, managed, and prioritised. These lessons shape how they save, spend, and plan as young adults and reduce the risk of impulsive spending or poor budgeting later.

Practical ways to teach smart money habits

Money lessons stick when they’re practical, not just theoretical. It’s about everyday moments, not long speeches.

1. Don’t hand over everything on demand: Even if you can afford what your child wants, don’t always buy it immediately. Not because you’re being strict, but because “not now” teaches patience, prioritization, and that wants don’t need instant fulfilment.

2. Link effort to reward: Tie small allowances or rewards to household chores. When they want something, encourage saving toward it. This shows the link between effort, earning, and spending and this builds discipline over time.

3.Teach saving as a habit, not a rule: Have children set aside a small portion of any money they get; birthdays, gifts from relatives, whatever. The amount matters less than consistency; saving becomes a reflex, not a punishment.

If you are holding it (as many African parents do), make it visible with a piggy bank or show them the account where the money is kept. It builds trust and awareness.

4. Teach wants vs. needs: Help them distinguish needs from wants, one of the most underrated money skills. It shapes lifelong decisions, especially when they start earning.

The home is the first classroom

Financial habits are caught more than they are taught. Children watch how you spend, save, and talk about money. If you preach budgeting but live impulsively, they’ll copy the behaviour, not the words.

The home sets the foundation. Schools, religious institutions, and even corporate organisations can complement this through financial literacy programmes and youth-focused initiatives

But family remains the strongest influence. In short: financially responsible kids need intentional role models.

Don’t just save: teach them to grow money

Saving is great, but keeping money under the mattress teaches the wrong lesson long-term. Over time, money loses value when it sits idle due to inflation. Introduce simple, low-risk options like high-yield savings or junior accounts to show money can grow.

This doesn’t mean turning children into mini investors. It simply means helping them understand that saving is step one but making money work wisely is the next level. This builds a healthier long-term mindset around patience, planning, and wealth-building.

The bigger impact on society

Teaching smart habits doesn’t just help individuals, it strengthens and shapes the society. Financially aware youths are less likely to fall into desperate financial decisions, fraudulent activities, or risky shortcuts like yahoo yahoo scams.

Over time, this leads to:

• Lower crime rates

• Reduced financial fraud

• More responsible consumer behavior

• A generation that plans, not just survives.

When people understand money, they control it not the other way around.

Why this matters

We teach kids money management not for overnight riches, but to spare them financial confusion, vulnerability, or debt cycles. Money will always be part of life, the real question is whether they’ll know how to manage it wisely. Catching them young isn’t pressure; it’s preparation.

In a world of costly mistakes, it’s the best gift.

Keep reading

Related Topics

Conversation

Comments (0)

Sign in to join the conversation or like this post.