Imagine lending money to a friend, but instead of hoping they pay you back, they guarantee to return your money with interest. Or picture lending ₦1 million to the Federal Government to build the Lagos–Ibadan highway, receiving steady interest every six months and getting your full amount back in 10 years.

Bonds are a foundational investment tool for anyone looking to preserve capital, earn steady income, or diversify their portfolio. Understanding how they work is essential, especially in markets like Nigeria, where bonds play a crucial role in funding government projects and corporate growth.

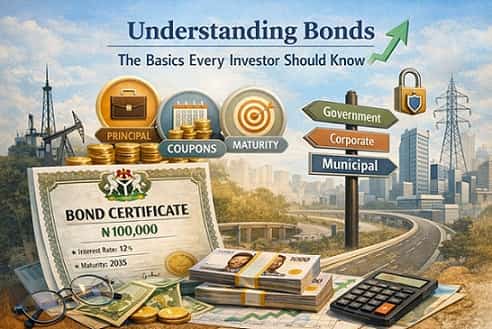

What Is a Bond?

A bond is a fixed-income security where you loan money to an issuer (such as a government, corporation, or state) for a set period. In return, you receive regular interest payments called coupons and your original investment (the principal) back at maturity.

Think of it as renting out your cash. The issuer pays “rent” (interest) until they return the house (your principal).

Unlike stocks, which give investors ownership in a company and the potential for higher returns (and higher losses) with long-term growth potential, bonds prioritize stability and capital preservation.

Who issues Bonds in Nigeria?

Several types of institutions issue bonds within Nigeria’s financial system.

1. Government Issuers

Federal Government of Nigeria (FGN Bonds): Issued by the Debt Management Office (DMO) to fund national infrastructure and manage government debt.

State Governments: States issue bonds to finance projects such as roads, hospitals, and public infrastructure. Many are backed by an Irrevocable Standing Payment Order (ISPO).

Local Governments and Agencies: Recent updates in Nigeria’s financial regulations allow local governments to issue municipal bonds for community-level projects.

2. Corporate Issuers

Companies issue bonds to raise funds for expansion, refinancing debt, or operational needs.

Corporate bonds typically offer higher yields than government bonds because they carry more risk.

3. Municipal / Sub-national Bonds

These bonds are issued by state or local authorities to finance infrastructure and development projects. They may be backed by government revenues or income from specific projects.

Nigeria’s bond market is overseen by the Securities and Exchange Commission (SEC), the Debt Management Office (DMO), and the Central Bank of Nigeria (CBN). Trading occurs on platforms such as the Nigerian Exchange (NGX) and FMDQ Securities Exchange.

How do Bonds work?

When you buy a bond, you are lending money for a defined period.

For example, you might purchase a bond with a face value of ₦100,000, earn 12% annual interest paid twice a year, and receive your ₦100,000 back when the bond matures.

Investors may buy bonds at face value, above face value (premium), or below face value (discount) depending on market conditions.

Key components of a Bond

1. Principal (Face value) is the amount originally invested, returned at maturity.

2. Coupon rate is the interest rate paid by the issuer.

3. Maturity date is the date when the principal is repaid.

4. Issuer is the entity borrowing the money (government, municipality, corporation).

How investors earn money

- Interest payments (Coupons): Regular income paid throughout the life of the bond.

- Capital gains: Profit earned if the bond is sold for more than the purchase price.

- Bond pricing: Bond prices change based on market conditions.

One important rule: Bond prices move opposite to interest rates.

If interest rates rise, older bonds paying lower interest become less attractive, so their prices fall. If interest rates fall, existing bonds with higher coupons become more valuable.

Premium bond: Coupon rate is higher than current market rates.

Discount bond: Coupon rate is lower than current market rates.

Types of Bonds in Nigeria

1. Government Bonds (FGN Bonds): Long-term securities issued by the federal government, typically with maturities between 5 and 30 years. They usually pay interest every six months and are considered the safest bonds in Nigeria.

2. Treasury Bills: Short-term government securities with maturities under one year. While technically money-market instruments, they are often grouped with bonds as fixed-income investments.

3. State and Municipal Bonds: Issued by state governments to finance infrastructure projects such as roads, hospitals, and schools.

4. Corporate Bonds: Issued by companies seeking funding for expansion or refinancing. These usually offer higher yields to compensate for higher risk.

5. Eurobonds: Bonds issued by Nigerian entities in foreign currencies such as US dollars. These can help hedge against naira depreciation.

6. Sukuk: Sharia-compliant investment certificates that provide returns through profit-sharing instead of interest.

7. Green bonds: Bonds issued to finance environmentally friendly projects such as renewable energy and climate initiatives.

Other variations include zero-coupon bonds, convertible bonds, callable bonds, floating-rate bonds, and retail savings bonds.

Benefits of investing in Bonds

Bonds play an important role in stabilizing an investment portfolio.

- Steady income: Regular interest payments provide predictable cash flow.

- Capital preservation: Bonds are generally safer than stocks and help protect invested capital.

- Portfolio diversification: They help reduce overall portfolio volatility when combined with equities.

- Lower volatility: Bond prices tend to fluctuate less than stocks.

- Potential tax advantages: Some bonds may offer tax benefits depending on structure and jurisdiction.

- Higher priority in bankruptcy: If a company fails, bondholders are typically paid before shareholders.

Because of these qualities, bonds are often favored by conservative investors or those approaching retirement.

Risks of Bonds in Nigeria

Despite their relative safety, bonds still carry risks.

1. Inflation Risk: High inflation can reduce the real value of interest payments.

2. Interest rate risk: Rising interest rates can lower the market value of existing bonds.

3. Currency risk (Eurobonds): Exchange rate movements may affect returns for Nigerian investors.

4. Credit or default risk: Corporate and some state bonds may fail to meet repayment obligations.

5. Liquidity risk: Some bonds may be difficult to sell quickly without a price discount.

6. Political and economic risk: Changes in government policy, oil prices, or economic stability can affect bond markets.

Risk by Bond type

FGN Bonds – Lowest risk

State Bonds – Moderate risk

Corporate Bonds – Higher risk

How to invest in Bonds

Investors can gain exposure to bonds in several ways.

- Individual bonds: These provide predictable income and defined maturity dates but may require larger capital and careful research.

- Bond funds or ETFs: These offer diversification across many bonds and are easier to access but fluctuate in value and charge management fees.

Where Nigerians can buy Bonds

• Through stockbrokers

• Through banks and asset managers

• Via bond funds and mutual funds

• Through primary auctions conducted by the Debt Management Office

• International investors may also use brokerage platforms such as Fidelity, Vanguard, or Schwab to purchase foreign bonds.

Key factors to consider

- Maturity: Short-term bonds carry lower risk, while long-term bonds may offer higher yields.

- Credit rating: Check ratings from agencies such as Agusto & Co.

- Yield to maturity (YTM): This measures the total expected return if the bond is held until maturity.

- Interest rate environment: Rising interest rates can reduce the value of existing bonds.

Conclusion

Bonds are one of the foundations of long-term investing. They provide steady income, help preserve capital, and bring stability to a portfolio.

Whether you are a beginner investor or someone looking to balance stock market risk, understanding how bonds work can significantly improve your financial decision-making.

Keep reading

Related Topics

Conversation

Comments (0)

Sign in to join the conversation or like this post.